That real harm will result from the use of AI tools is a given.

The rot caused by easy money will only become fully visible when the hollowed out institutions start collapsing under the weight of incompetence, debt and hubris.

We have yet to reach a full reckoning of the consequences of the era of easy money, but it’s abundantly clear that it ruined us. The damage was incremental at first, but the perverse incentives and distortions of easy money–zero-interest rate policy (ZIRP), credit available without limits to those who are more equal than others–accelerated the institutionalization of these toxic dynamics throughout the economy and society.

Fifteen long years later, the damage cannot be undone because the entire status quo is now dependent on the easy-money bubble for its survival. Should the bubbles inflated by easy money pop, the financial system and the economy will collapse into a putrid heap, undone by the perversions and distortions of endless easy money.

Easy money created destructive, mutually reinforcing distortions on multiple fronts. Let’s examine the primary ways easy money led to ruin.

1. The near-zero rate credit was distributed asymmetrically; only the wealthiest few had access to the open spigot of “free money.” The rest of us saw mortgage rates decline, but we were still paying much higher rates of interest than corporations, banks and financiers.

If we’d all been given the opportunity to borrow a couple million dollars at 1% and put the easy money into bonds yielding 2.5%, skimming a low-risk 1.5% for producing nothing, we’d have jumped on it. But that opportunity was only available to banks, the super-wealthy, corporations and financiers.

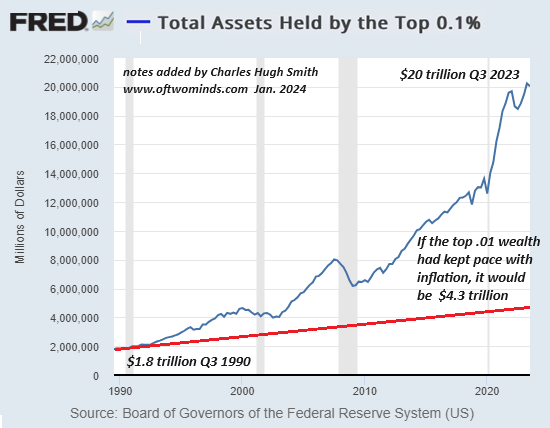

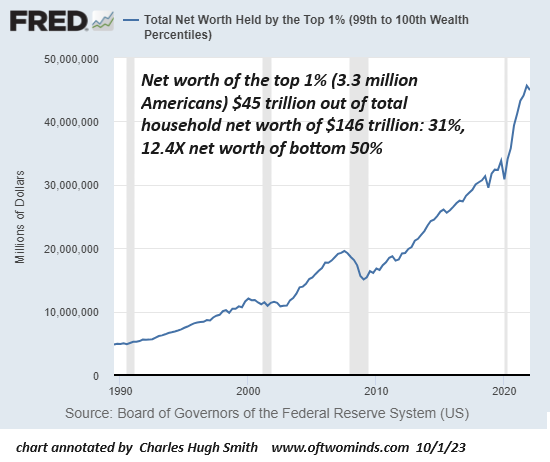

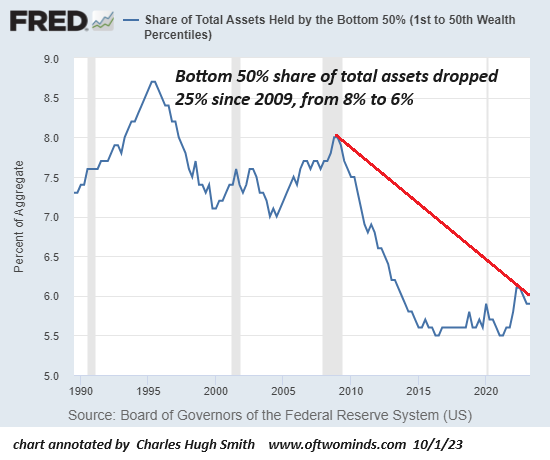

The charts below show the perverse consequences of offering the wealthiest few limitless money at near-zero rates while the rest of us paid much higher interest. The wealthiest few could buy income-producing assets on the cheap at carrying costs no ordinary investor could match. Since there was so much “free money” sloshing around for financial elites to tap, the demand for income-producing assets soared, pushing prices into the stratosphere. These enormous increases in valuation generated stupendous capital gains for the wealthiest few.

Look at 2009 as the starting point in these charts, as that’s when the Federal Reserve instituted ZIRP and opened the spigots of easy money to “those with first access,” i.e. banks, corporations and financiers.

Here we see how the assets of the top 0.1% more than tripled since 2009, far outpacing inflation.

The net worth of the top 1% went ballistic as well. Nearly free credit is rocket fuel if you’re first in line and nobody else gets the same interest rate.

The bottom 50% of American households lost ground in the era of easy money. This is not coincidence, it’s direct causation: give the lowest interest rates and unlimited credit to the wealthy, and they will buy up the most productive assets, leaving crumbs for the rest of the American citizenry.

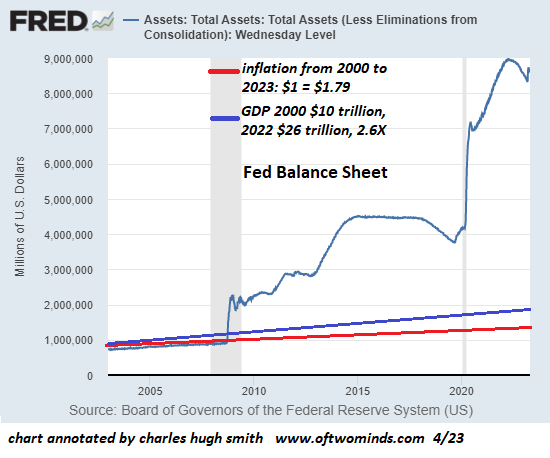

Here’s the Fed balance sheet, the money they created out of thin air and injected into the cheap-unlimited-credit-for-the-wealthy machine.

Note how the easy money sparked federal borrowing. Federal debt was under the line of GDP expansion until 2009, at which point it took off in a parabolic ascent. Now that interest rates have finally normalized a bit, the gargantuan interest on this debt will be extracted from the citizenry via higher taxes and/or reduced federal spending. (Giveaways to wealthy political donors will of course remain untouched, along with tax havens for the super-wealthy.)

The social perversions of easy money are equally destructive. When it’s cheap and easy to borrow more money, that becomes the “obvious” way to deal with challenges. This incentivizes enterprises and institutions to advance those with skills in finance and PR rather than in management.

With the discipline imposed by the cost of money gone and the expansion of opportunities to reap fortunes by pyramiding credit and leverage, competency was redefined from management focused on increasing productivity and cutting costs through efficiencies to extracting the soaring value of existing assets: nothing new was produced but yowza, a lot of people sure got rich.

The rot created by easy money has seeped into every fiber of our social, political and economic orders. Correspondent D.T. drew a direct line between easy money and the decline of competence in The Powers That Be:

“Nepo(tism) babies selected by accident of birth without any tempering in flames… cocooned in their own reality, disdainful of the unselected, coddled and hothoused, ignorant of history and, worst of all, supremely confident in the superiority of their own righteous abilities… because when you get first dibs on the free money there are no consequences you can’t buy your way out of.”

Is there any doubt that what some are calling The Disconnected Elite (DE) have fortified their Ivy League-luxe-enclave bubbles and unearned privileges with the easy money that comes with their position atop the heap? The cost of this elevation of incompetence, the complete disconnection from the realities of everyday Americans and the hubristic confidence in their own talent–i.e., believing your own PR–has hollowed out the nation’s institutions in ways those outside the institution cannot yet observe.

The rot caused by easy money will only become fully visible when the hollowed out institutions start collapsing under the weight of incompetence, debt and hubris.

New podcast:

Self Reliance (45 min).

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Inform Passion ($1/month), for your most generous subscription |

Thank you, Ignacio M. ($5/month), for your marvelously generous subscription |

|

|

Thank you, Kenneth C. ($100), for your outrageously generous contribution |

Thank you, Kheng L.T. ($50), for your magnificently generous Substack contribution |

The mainstream holds the Fed is busy planning a return to the glory days of zero interest rates, but ZIRP is on the downside of the S-Curve; it’s done, gone, history.

Speculation has its own expiration dynamics, and they don’t depend on us recognizing speculative excess for what it is. They will unravel the excesses regardless of what we think, hope or deny.

Economists and pundits steer well clear of the eventual social and political consequences of America’s entrenched neofeudal wealth-income inequality.

Now that debt is rising faster than “growth,” and “growth” is dependent on speculative credit-asset bubbles, the collapse of the Keynesian dream looms large.

We either make the future or break the future, so choose wisely.

There is a make-or-break financial fork in the road ahead for the United States: there are only three options:

1. Slash trillions of dollars in annual federal spending to align with current tax revenues.

2. Raise trillions in additional tax revenue from the only entities able to pay more, corporations and the top 5%

3. Monetize the soaring federal debt by the central bank “printing money” and using this new money to buy Treasury bonds, as issuing new Treasury bonds for sale is the way the federal government funds its stupendous deficit spending.

One approach might be to do some of each, but there are political obstacles to any rational response to unsustainable federal debt expansion.

Any cuts in spending large enough to be consequential will slash-and-burn either the cash overflowing in the federal trough that politically powerful cartels are gorging on, or entitlements that buy the complicity / passivity of the general populace. Neither is politically viable.

Those who can afford to pay more taxes–corporations and the top 5%–are (surprise) the most politically powerful groups in the nation, and they will never accede to tax increases high enough to be consequential.

Politically, the only viable option is the politically painless one of monetizing the soaring federal debt via the Federal Reserve creating $2 trillion a year with a few keystrokes and using this $2 trillion to buy virtually all the newly issued Treasury bonds.

If private owners of existing Treasury debt find the yield they’re receiving doesn’t even keep up with inflation, they will sell their Treasuries, forcing the Fed to print additional trillions every year to monetize portions of the existing $30 trillion in debt.

Recall that a significant percentage of state and local government spending is funded by the issuance of municipal bonds. This other governmental debt competes with Treasury issued bonds for scarce private capital. Other nations’ bonds are also competitors for private capital.

Since capital flows to the highest and lowest-risk yields, yields have to rise to attract private capital.

This creates another problem: as yields rise, so does the interest paid on the entire portfolio of bonds.

Higher interest payments then pressure other government spending. The politically painless solution is to monetize not just the newly issued debt but the rising interest payments due on the soaring debt.

Monetizing government debt is what I call the perpetual money motion machine. Just create another trillion to buy newly issued bonds, an additional trillion to pay higher interest and more trillions to buy up old debt that private owners are selling.

Is there anything that could break the perpetual money motion machine? Those pointing to Japan’s deflationary stagflation of the past 30+ years claim there are no impediments to ever-greater monetization. The Federal Reserve can expand its balance sheet by $10 trillion or $50 trillion without any structural problems arising.

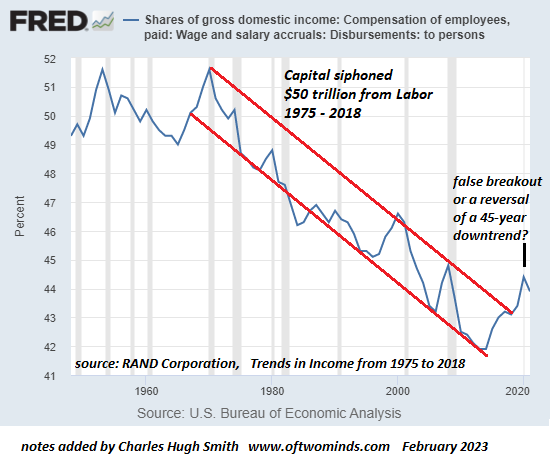

Interesting, that $50 trillion number. That’s the amount that the top 5% skimmed from labor in the past 45 years.

The Bill for America’s $50 Trillion Gluttony of Inequality Is Overdue (September 21, 2020)

Trends in Income From 1975 to 2018 (RAND Corporation)

Setting aside the political veto of the wealthiest corporate interests and households, clawing back this $50 trillion via higher taxes on those who gained the $50 trillion would be karmic justice and present fewer risks that the insane scheme of just “printing more money” to satisfy every cartel, entrenched interest and entitlement.

Let’s ask a simple question of history: if monetizing debt works so wondrously, why hasn’t it been the go-to solution for every free-spending government? In the good old days, creating money out of thin air was accomplished by replacing the silver or gold in coins with lead or other base metals.

Alas, people catch on to this devaluation of money, and inflation skyrockets accordingly. Proponents of adding $50 trillion to the Fed’s balance sheet (i.e. monetizing the soaring debt and interest payments) claim this hocus-pocus won’t spark inflation. But since all that newly issued currency enters the economy one way or another, how can it not generate inflation?

The status quo answer is: if it only inflates assets owned by the wealthy, that inflation is really rather grand.

But suppose inflation leaks into Cheetos instead of Big Tech stocks? Since “We can’t eat iPhones,” that eventually matters.

In other words, there is a governor built into the perpetual money motion machine: real-world inflation.

There is also a social governor built into the “painless” expansion of asset bubbles that favor the already-wealthy: eventually this systemic inequality distorts and destabilizes the social and economic order.

This in one reason why history shows government debt in excess of 100% of GDP (the real economy) eventually leads to disorder, default and bankruptcy. Or revolution. Take your pick. (Chart courtesy of David Sommers.)

If $50 trillion were clawed back from the wealthiest corporations and households, that would only return total assets owned by the wealthy to levels that were considered excessive a decade ago. But since this is politically unviable, the “painless” option of monetizing debt will be pursued.

But since the only possible outcomes of this option are disorder, insolvency or revolution, the wealthy may well regret their short-sighted greed. Nemesis can take various forms, but eventually the pendulum swings from one extreme (monetary hocus-pocus and staggering inequality) to the other extreme (clawback of central-bank-bubble “wealth” and a balance of revenues and expenditures).

The meteor that will obliterate the financial hocus-pocus is already visible and cannot be diverted by dancing the humba-humba and waving dead chickens around the campfire, i.e. Federal Reserve policies. Claiming god-like powers doesn’t grant one god-like powers.

There’s no going back once we select a pathway. The systemic damage cannot be reversed, regardless of what happy stories are told around the campfire by credulous believers in the magical powers of waving dead chickens around. We either make the future or break the future, so choose wisely.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, newbs3247 ($50), for your splendidly generous Substack subscription |

Thank you, starucca ($5/month), for your superbly generous Substack subscription |

|

Thank you, bpodkulski ($5/month), for your superbly generous Substack subscription |

Thank you, mcbride ($50), for your outstandingly generous Substack subscription |

Blowback has its own dynamics, as we’ll learn in the decade ahead.

One of the most durable expectations in the financial sphere is that inflation will drop sharply in a recession and the Federal Reserve will lower interest rates back to near-zero. There is a good reason to doubt this: rising wages. Yes, we all hear about the millions of human workers who will shortly be replaced by AI–wonderful for corporate profits!–but few pundits bother looking at long cycles in interest rates and inflation, and even fewer pay any attention to the absurdly extreme asymmetry of labor and capital.

As I’ve often noted here, labor’s share of the economy has fallen for 45 years. Only recently did it reverse slightly. It’s not yet clear if this was a brief false-breakout ot a change in trend, but there are good reasons to expect a secular, cyclical reversal that lasts years or even a decade.

In other words, a decade in which labor / wages gain at the expense of capital.

There are two basic narratives that are offered as explanations for how capital siphoned $50 trillion from labor over the last 45 years. One is that the macro-forces of globalization and financialization inherently favor capital and reduce labor’s leverage as production and jobs were offshored and US workers entered a race-to-the-bottom competition with developing nations’ low-cost workforces–a competition that kept US wages stagnant even as US corporate profits and financial assets soared.

The other narrative starts with the observation that the erosion of wages and the glorification of corporate power was the direct result of specific policies being adopted.

The dominance of corporate interests and the stripmining of labor were anything but inevitable: it was

engineered by policies that enriched the top 0.01% (the Financial Aristocracy), and the

top 10% who own 90% of America’s productive capital.

This wholesale transfer of wealth and income from workers to Capital was documented

by a RAND Corporation report,

Trends in Income From 1975 to 2018.

Time magazine summarized the findings:

The Top 1% of Americans Have Taken $50 Trillion From the Bottom 90% —

And That’s Made the U.S. Less Secure.

(We’re told the stagnating wages of the past 45 years) were the unfortunate but necessary price of keeping American

businesses competitive in an increasingly cutthroat global market. But in fact, the $50 trillion

transfer of wealth the RAND report documents has occurred entirely within the American economy,

not between it and its trading partners. No, this upward redistribution of income, wealth, and

power wasn’t inevitable; it was a political choice–a direct result of the trickle-down policies we chose

to implement since 1981.

The net result of this four-decade siphoning of wealth/income from workers was

documented by a Foreign Affairs article:

Monopoly Versus Democracy:

Ten percent of Americans now control 97 percent

of all capital income in the country. Nearly half of the new income generated since the global

financial crisis of 2008 has gone to the wealthiest one percent of U.S. citizens.

The richest three Americans collectively have more wealth than the poorest 160 million Americans.

In other words, the bottom 90% have very little stake in the status quo: they receive

essentially zero income from America’s stupendous $140 trillion hoard of private wealth and

have essentially zero political influence, as documented in

Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens.

We can see these realities in the data /charts.

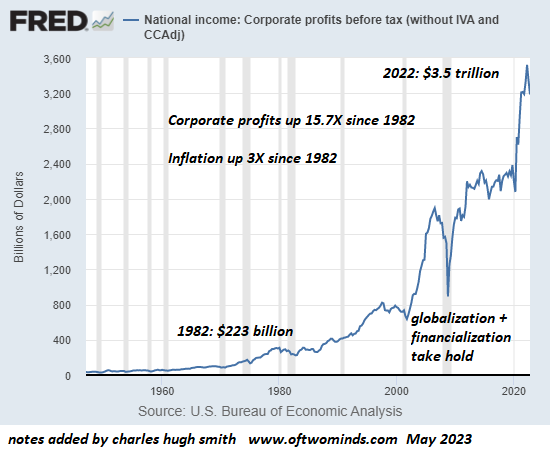

As the charts below (courtesy of the Federal Reserve FRED database) show, wages’ share topped out in the early 1970s and trended down for 45 years. Corporate profits skyrocketed 15.7-fold since 1982 while inflation rose “only” 3-fold.

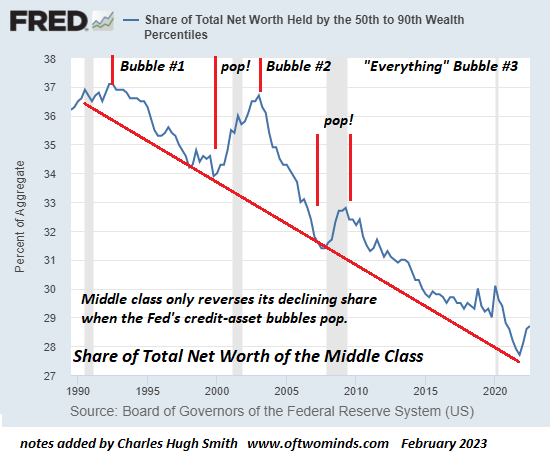

This decline in wages is mirrored by a corresponding decline in the wealth of the bottom 90%. It’s not just wages that stagnated–so did the share of the nation’s wealth held by the middle class / bottom 90%.

The middle class’s share of private-sector wealth (total net worth) has plummeted from 37% in the early 1990s to 28%, a decline of $12 trillion compared to what would have been the case had the middle class continued to hold 37% of net worth.

$50 trillion here, $12 trillion there, pretty soon you’re talking real money that’s been transferred from the wage-earning peasantry to America’s Financial Aristocracy.

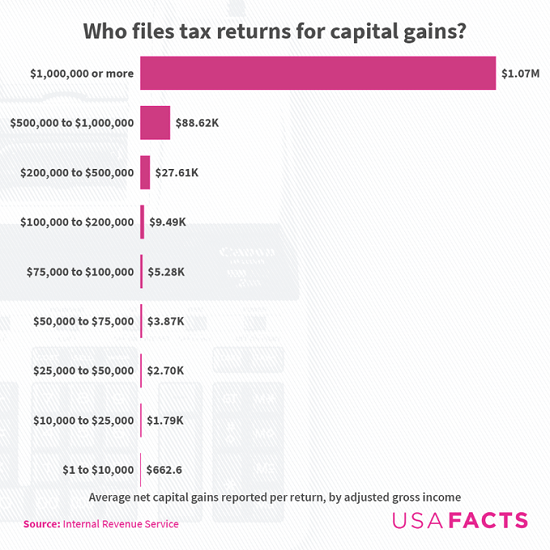

We see this vast asymmetry in who collects the primary engine of wealth for the top few: capital gains. Those who already own most of the wealth have pocketed the stupendous gains of the past three decades.

Middle class households pocket $4,000 or $5,000 in annual capital gains while those who own most of the wealth pocket on average a cool $1 million–200 times the middle class gain in unearned income.

So why will wages rise, regardless of deflation and AI? Catch-up and blowback. Even if we accept the “gee, we were helpless to stop wage stagnation” story (which is false, as detailed above), financialization and globalization are reversing and so labor can finally play catch-up to capital’s asymmetric gains.

If catch-up is suppressed by corporate political power, then blowback kicks into gear. The workforce has had enough of corporate-state pillaging, and while corporations are gleefully planning the elimination of their human workforce via AI and automation, that fantasy isn’t going to play out as expected, for automation has limits which I discuss in my book

Will You Be Richer or Poorer?.

Nobody thinks that there could be political limits on corporate power, but precious few asymmetries that reward the few at the expense of the many last forever. Blowback has a remarkable ability to careen from nobody notices or cares to full-blown revolt in relatively short order. The greater the asymmetry, plunder and hubris of the Aristocracy, the greater the eventual swing of the pendulum to the opposite extreme. Blowback has its own dynamics, as we’ll learn in the decade ahead.

Wages–and the inflation they generate–are going up for good whether anyone thinks this is possible or not. And inflation pulls interest rates higher, whether anyone thinks this is possible or not. It’s not just the Federal Reserve that matters; asymmetries, exploitation and plunder matter, too.

New Podcast:

Its a Waterfall – Risk, Collateral & Productivity (48 min)

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, James N. ($50), for your extremely generous contribution |

Thank you, Michael T. ($35), for yet another marvelously generous contribution |

|

Thank you, Ciprian M. ($54), for your splendidly generous contribution |

Thank you, David W. ($40), for your superbly generous contribution |

When we lose small businesses, we lose More than tax revenues.

Small businesses receive plenty of lip service but very little appreciation–until they’re gone. By then it’s too late to do anything but mutter, “you don’t know what you’ve got until it’s gone.”

Small businesses aren’t just sources of tax revenues, they’re sources of a wide range of jobs that can’t be replaced by Corporate America or the government. Just as importantly, small business owners and entrepreneurs are advocates for the neighborhoods, districts and cities they depend on for customers and suppliers.

The livelihoods of the owners and their employees depend on maintaining the viability of their neighborhood / district / city, which includes public safety and services such as transportation and trash collection, and a minimum density of other private-sector services and amenities which provide residents a safe, appealing atmosphere worth visiting.

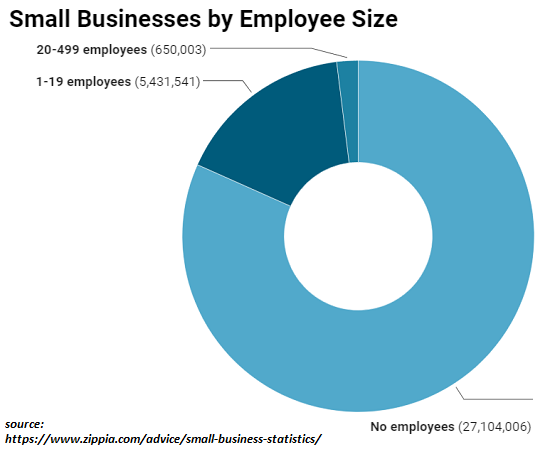

59.9 million Americans work at small businesses across the nation.

An estimated 47% of Americans shop at small businesses at least twice a week, generating about 45% of the nation’s economic activity.

According to the most recent available numbers from the U.S. Census, approximately 47% of U.S. employees work for small businesses, compared to 54.5% in 1988.

Small business entrepreneurs are risking everything they have to open and operate a business. They have far more skin in the game than city functionaries tasked with enforcing regulations and collecting business-related fees or their employees, who have the freedom to quit and seek employment elsewhere.

Residents tend to feel powerless to stop the decay of their neighborhood safety, services and amenities. They tried contacting their elected officials or municipal functionaries and were given a meaningless feel-good reply which everyone involved knows is empty.

Small business owners are more willing to apply meaningful pressure because they know the decay follows a sobering slide in which incremental declines pile up and eventually trigger a phase change in which the character of the neighborhood / district / city goes over a cliff no one discerned: petty crime increases, paving the way for more serious crimes to proliferate; customers thin out and then become scarce, and the zeitgeist goes from friendly to wary to unpredictable or even dangerous.

The core characteristic of of neofeudal economy and society is that it’s two-tier: there are two tiers of “criminal justice,” one of wrist-slaps and vast white-collar crimes ignored for elites and the wealthy, and another far more brutal and Kafkaesque for the rest of us.

In terms of commerce, Big Tech is free to establish monopolies and Finance escapes all the supposed regulatory safeguards, while small business is throttled with endlessly multiplying petty regulations that have little or nothing to do with public safety or employee labor rights. Corporate America has the immense wealth and power to gut any regulations it finds onerous, but small business struggles to pay the soaring costs of compliance and the tripling of junk fees such as business license renewals.

City-provided services degrade but the costs for the privilege of doing business triple.

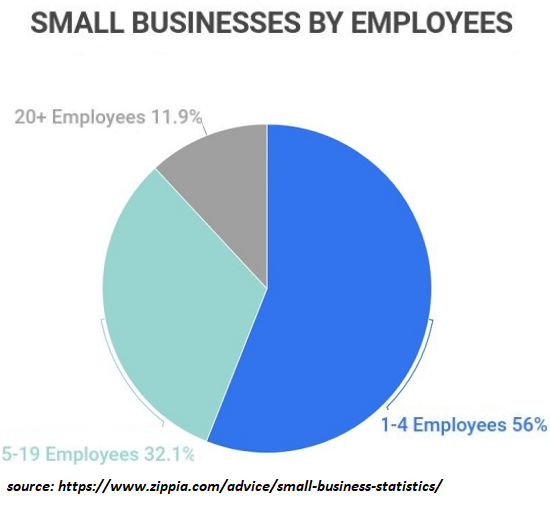

The majority of small businesses are sole proprietors. (see chart below) Many of these are online or at-home enterprises that are invisible to residents walking down the sidewalk. The 5.4 million small businesses with less than 20 employees are visibly consequential to the viability of bricks-and-mortar neighborhood commerce.

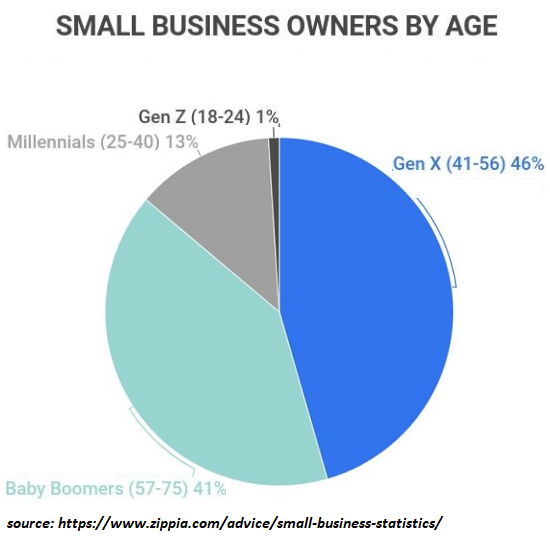

Demographics play a large role in the viability of small businesses. About 40% of all small businesses are owned by Boomers nearing retirement or already past the age of typical retirement. It won’t take much in the way of losses or stress to nudge these owners into selling or closing the business.

But if conditions are decaying, who’s going to buy a struggling business? The grim reality is “no one.” Owners are already working long hours and enduring high levels of stress. This self-exploitation can only go so far before the owners’ health and/or finances break down in burnout or losses.

Municipal bureaucracies tend to see small business tax donkeys as something they can count on much like a gushing spring. Should one tax donkey collapse and close a business, another tax donkey will magically appear to pick up the self-exploitation harness and start a new business in the same space.

Local-economy boosters love to cite the flood of new business applications as proof the spring is still gushing, but many of these new enterprises are sole proprietorships with no storefront presence and no employees. Many new businesses that thrived in the post-pandemic boom will soon encounter the headwinds of recession for the first time, and many will find their enterprises blown onto the unforgiving rocks of financial losses.

The phase-change shift in the character and zeitgeist of neighborhoods, districts and cities is difficult to reverse.

Once people no longer feel safe, they won’t come back. Once the empty storefronts and homeless encampments dominate the landscape, they won’t come back. Once services deteriorate and trash accumulates, they won’t come back.

Municipal bureaucracies are largely staffed by people who have never experienced what a real recession (such as 1981-2) can do to commerce, tax revenues and small businesses struggling to survive. They’re confident that history demonstrates any downturn will be brief and the tax donkeys will appear as usual to fill the empty storefronts, lofts and offices.

But this time will be different. No new tax donkeys will appear to gamble their fortunes and lives on starting a stupidly expensive-to-operate business, pay prevailing wages and benefits and all the taxes, licenses and junk fees municipalities have piled on small business.

When we lose small businesses, we lose more than tax revenues. We lose the engines of employment and the commercial foundation of neighborhoods and districts. When these foundations crumble, those residents who see the slide down the slippery slope of decay sell their homes and get out while the getting’s good. Those who remain will regret their inaction.

Tax donkeys don’t appear by magic. There has to be an infrastructure in place that allows a real opportunity to scrape out a living despite the high costs and formidable challenges. If the infrastructure and character of a place decay, so does the opportunity, and small businesses melt into air when it’s longer worth the struggle.

New Podcast:

Its a Waterfall – Risk, Collateral & Productivity (48 min)

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Thomas W. ($50), for your splendidly generous contribution |

Thank you, David A. ($50), for your superbly generous contribution |

|

Thank you, Thomas H. ($10.80), for your most generous contribution |

Thank you, Robert W. ($15), for your remarkably generous contribution |

Extremes keep getting more extreme, but for those at the top of the heap, it’s all fine. For everyone else slipping down the ladder, all that FINE adds up to Fragile, Insecure, Nonsensical, Expensive.

Readers occasionally point out I’ve been predicting that unsustainable extremes will eventually unravel for 10+ years, yet everything’s still fine. Yes, everything’s still fine, maybe even peachy, but perhaps we should describe “fine” in light of the policy extremes that keep getting more extreme to keep all that fineness duct-taped together.

How about this for FINE:

Fragile

Insecure

Nonsensical

Expensive

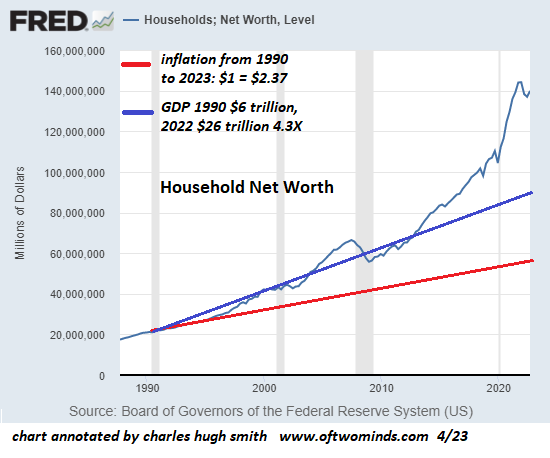

To assess just how extreme things have become beneath the placid surface of peachiness, let’s look at federal debt, the Fed balance sheet and Household Net Worth in relation to inflation and GDP, two standard measures of growth.

All else being equal, most economic-financial metrics will roughly track either inflation or Gross Domestic Product (GDP), the broad measure of the economy’s activity / expansion /contraction.

In other words, one way to identify extremes is to look for metrics that are way out of line with GDP and inflation.

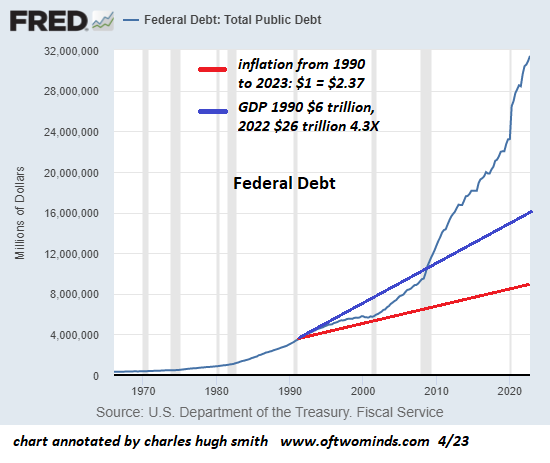

Consider federal debt as an example. We can be forgiven for assuming federal borrowing would more or less track the expansion of GDP.

But as the chart below shows, if federal debt had tracked GDP since 1990, it would be around $16 trillion, half of its current bloat of $32 trillion. Hmm, $16 trillion here, $16 trillion there and pretty soon you’re talking real money.

The GDP of Japan is around $4.3 trillion, the GDP of Germany is about $4 trillion, so that $16 trillion in “excess federal borrowing and spending” is the equivalent to four GDPs of the third and fourth largest economies in the world (just behind the US and China).

Does an “excess $16 trillion” of federal debt qualify as extreme? I think the fair conclusion is “yes.”

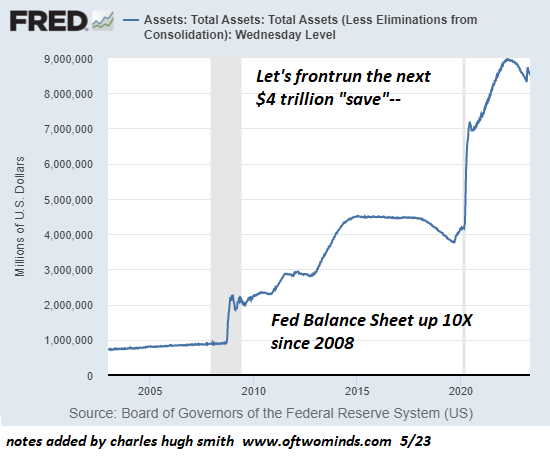

Next up, the Federal Reserve Balance Sheet, which reflects the sum created out of thin air to buy US Treasury bonds and mortgage-backed securities as the means to inject gobs of US dollars into the financial system as liquidity for speculation.

Hmm, if the Fed balance sheet had tracked GDP, it would have risen from around $700 billion in the early 2000s to a meager $1.8 trillion, a far cry from its current level of $8.6 trillion. In round numbers, this is about $7 trillion in “excess Federal Reserve stimulus,” not quite the combined GDPs of Japan and Germany but hey, $1 trillion at these levels is a mere rounding error, right?

Now let’s look at the really, really fine part of the extremes, Household Net Worth: all the plump, juicy wealth created for the top 10% who own the vast majority of financial assets to enjoy.

If Household Net Worth had tracked GDP, it would total about $90 trillion, $50 trillion less than its current level of $140 trillion. You see what’s really fine here: the federal government injects $16 trillion in excess stimulus, the Federal Reserve injects $7 trillion in excess stimulus for a total of $23 trillion, and the top 10% reap $50 trillion in excess wealth: yowza, that’s a really fine investment!

Of course private and corporate debt has soared along with federal debt, but never mind the details. $50 trillion in excess wealth is roughly twice the size of America’s GDP of $26 trillion. That’s a lot of extremely fine wealth to play with.

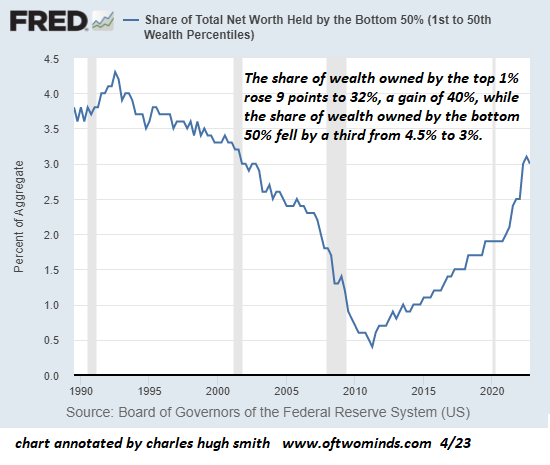

But all this really fine wealth hasn’t exactly been evenly distributed. It turns out the bottom 50% of households lost ground since 1990, as their share of the total household wealth fell from about 4.5% to 3% (see chart below).

The middle class (the 50% to 90% segment of households) also lost ground, as their share of wealth fell from above 36% to less than 29%. A 7% decline may not sound like much, but recall that each 1% is $1.4 trillion, so that 7% decline adds up to roughly $10 trillion in today’s total wealth of $140 trillion.

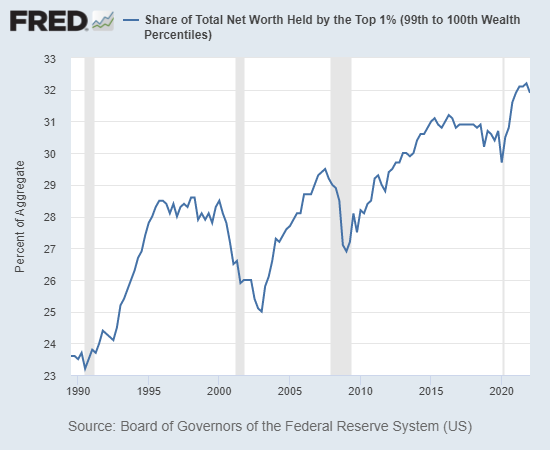

Meanwhile, back at the Really Fine Ranch, the top 1% saw its share of the wealth soar by 40%, from 23% to 32%.

It seems some have received more fineness than others.

Extremes keep getting more extreme, but for those at the top of the heap, it’s all fine. For everyone else slipping down the ladder, all that FINE adds up to Fragile, Insecure, Nonsensical, Expensive.

New Podcast:

Its a Waterfall – Risk, Collateral & Productivity (48 min)

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can’t Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Cozmin L. ($100), for your outrageously generous contribution |

Thank you, Roy P. ($5/month), for your monstrously generous pledge |

|

Thank you, Sebastian S. ($40), for your magnificently generous contribution |

Thank you, Jeffrey N. ($50), for your superbly generous contribution |