Rupert Murdoch’s News Corp. owns the Wall Street Journal and the housing marketing service Move Inc. Move Inc.’s main client is the National Association of Realtors. In sisterhood with Move, the newspaper is prone to printing outright, bald-faced lies about the state of the housing market in the US, whenever it thinks it can get away with it. And since nobody is paying attention, it gets away with it.

Yesterday it printed another whopper on the subject of the NAR’s “existing home sales” print for May. The Journal said, “Sales last month hit their strongest pace since November 2009.” That’s simply false. I’ll get to that in a minute.

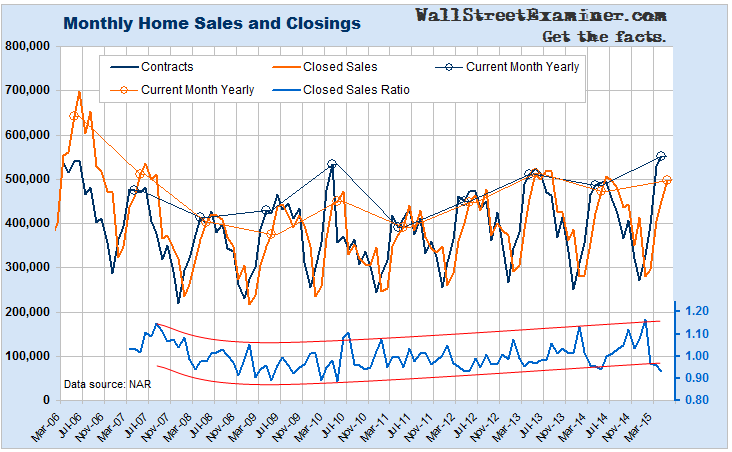

Aside from the fact that the Journal reported a figure which was false, this isn’t actually sales data. It’s the number of sales that were settled that month. The sales took place a month or two earlier. This is like if retailers reported sales when customers paid their credit card bills a month or two after the actual purchase. Like all retailers, the monumentally monolithic NAR cartel has the actual data on the closing of the contracts at the time they occur, but it refuses to report it.

The national online real estate brokerage Redfin gives us the facts by reporting contract agreements (which the NAR calls “pending home sales”) for 58 US metros a few weeks after the fact, using the NAR’s MLS databases. This data showed that sales rose 3.1% year over year in May. That compares with the NAR’s reported 9.2% gain in May year over year sales using a grossly faulty seasonal adjustment factor. The NAR’s actual data, not seasonally adjusted, on closings (“existing home sales”) showed that the year to year gain was 5.1%. Even though that may have been the correct figure for closings, Redfin’s data for contracts signed in May at +3.1% shows that the market appreciably slowed since NARs reported “sales” were contracted in March and April.

April may have been when the housing market reached peak momentum. Mortgage rates were near their lowest levels in 2 years in March and April. Since then mortgage rates have spiked.

The biggest problem may be with the statement, which WSJ made up, that sales had reached their “strongest pace” since November 2009. Considering just the NAR’s actual, not seasonally finagled data, there were 497,000 “sales” in May. In May of 2013 there were 514,000 sales. In fact, in every month this year except February when mortgage rates were at their lowest point, existing home sales were below the same month’s levels in 2013.

In fairness to the NAR and the Journal, which actively promotes its affiliated housing business via the newspaper, April contracts were at the highest level since the recovery. That brings up another problem. Since May closings did not keep pace with April’s contracts, contract fallout increased and the ratio of closed sales to prior contracts fell to 93.2%, the lowest level since 2012. That broke an improving trend that had been under way since the bottom of the housing crash.

Is that a canary in the coal mine? It’s logical that there would be some sensitivity between contract failures and rising mortgage rates. Most buyers in the housing market are on the bubble to begin with. They simply cannot afford higher rates at these price levels. Something has to give. If mortgage rates rise from here, will it be sales volume, or house price inflation (now around 8%), or both?

Meanwhile, the Wall Street Journal pretends to be an unbiased news organization as it continues to report NAR data while acting as a PR firm for its sister company, MOVE Inc. It’s an outrage. But other paid observers (formerly known as journalists or reporters) continue to sleepwalk through this data every month too. All of the mainstream media organizations and their employed lackeys are on the take from the housing industry. They cannot, and will not, report the data without gross bias.

Join the conversation and have a little fun at Capitalstool.com. If you are a new visitor to the Stool, please register and join in! To post your observations and charts, and snide, but good-natured, comments, click here to register. Be sure to respond to the confirmation email which is sent instantly. If not in your inbox, check your spam filter.

{kind=link}

Nick Timiraos of the WSJ is arguing that because May had fewer biz days than last year, it should be adjusted.

Nick is a nice guy, but he’s never worked in real estate, and I get the feeling that he has never actually spoken to a real estate salesperson. Probably not true, but his argument makes it seem so. On the other hand I was a Realtor many years ago. I also was a mortgage broker. My family has been in the real estate business for 100 years. I also spent 15 years as a commercial appraiser and had a bit of interaction with residential sales people there as well. So I have first hand experience with this.

The business of selling houses goes on every day of the month. Closings are heaviest at the end of the month. Indeed, they are virtually always held on business days. Timiraos is arguing that because of that, sales in May this year were suppressed. But the fact is that regardless of whether the last business day of the month is the 29th, 30th, or 31st, people who want to close in May will close in May. Ask around to the title companies, Nick. They’ll tell you how busy they were the last few days of May. They got the deals done in that month.

For that matter, January, March, and April closings were all lower in 2015 than 2013. Only February, when rates were rock bottom, saw higher sales.

The most important fact in all this is the increase in the fallout ratio. That may well be the first indication that the top of the cycle is in.