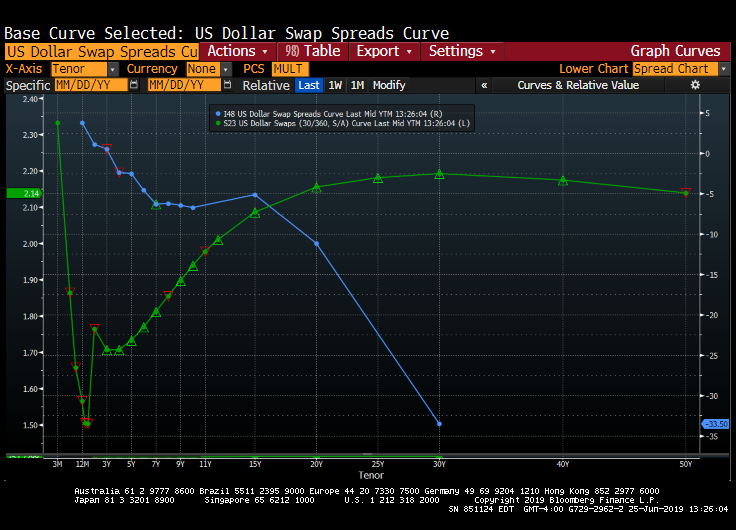

As central banks like the US Federal Reserve try to counter a sagging global economy (and preserve asset bubbles), strange things begin to happen. Like the US 2-year swap spread going negative for the first time ever!

(Bloomberg) — The U.S. 2-year swap rate moved below the 2-year Treasury note’s yield for the first time ever Tuesday after 3-month dollar Libor’s latest drop, turning the 2-year swap spread negative. It was the last tenor on the swap spread curve to fall below zero.

Currently around -0.25bp, 2-year spreads dropped as low as -0.5bp, tighter on the day by 1bp; spread is tighter by ~12.5bp since the start of May

- 3-month dollar Libor fixed lower by 2.16bp at 2.31125 Tuesday, lowest since August 2018

- A combination of higher general collateral rates, overseas selling and hedging flows have weighed on front-end spreads over the past couple of months;

Here is the US Dollar Swap Curve and the Swap Spread curve.

Join the conversation and have a little fun at Capitalstool.com. If you are a new visitor to the Stool, please register and join in! To post your observations and charts, and snide, but good-natured, comments, click here to register. Be sure to respond to the confirmation email which is sent instantly. If not in your inbox, check your spam filter.