Bankers dumping business loans and corporate debt in the forms of Collateralized Loan Obligations off on investors in the US and Europe? As New York Yankee legend Yogi Berra once said, “It’s déjà vu all over again.”

The year’s first batch of new CLO issues to price in the U.S. includes two transactions with short maturities and one static deal, where the underlying pool of loans remains the same throughout its lifetime. These non-typical features are offered to draw in investors some of who have grown more cautious after leveraged-loan prices dropped and CLO funding costs rose at the end of last year.

Investors say similar structures are being touted in Europe as well. And it’s not the first time that more creative structures have appeared: short-dated deals emerged in 2015 and 2016 when market conditions deteriorated during the oil and gas crisis and liability spreads ballooned.

Issuance of CLOs — bonds whose cashflows are provided by an underlying pool of loans — soared last year as investors wanted exposure to higher-yielding, floating-rate debt. The market stalled toward year end amid the broader market volatility and weaker sentiment. CLO managers are now trying to navigate the slow recovery in the market.

*Pine Bridge Capital has a nice “CLOs for Dummies” article.

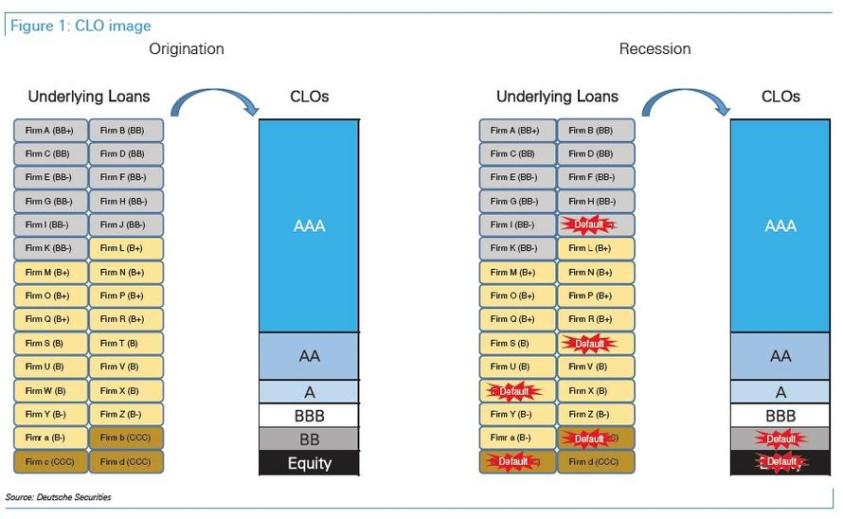

Although CLOs are primarily bank and corporate loans, they can degrade quickly like the “subprime” loans in 2008/2009 (as discussed in The Big Short somewhat accurately).

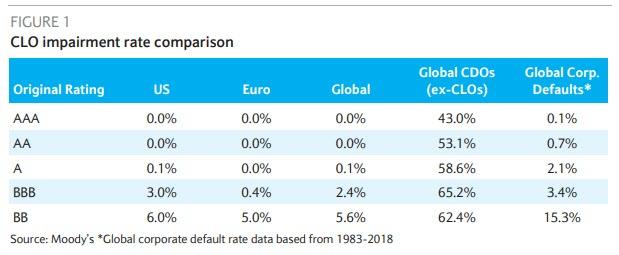

And like the period of time discussed in The Big Short (and other lated books and movies), the “A” rated tranches are looking good in terms of impairment rates, but the “killler Bs” are looking stressed.

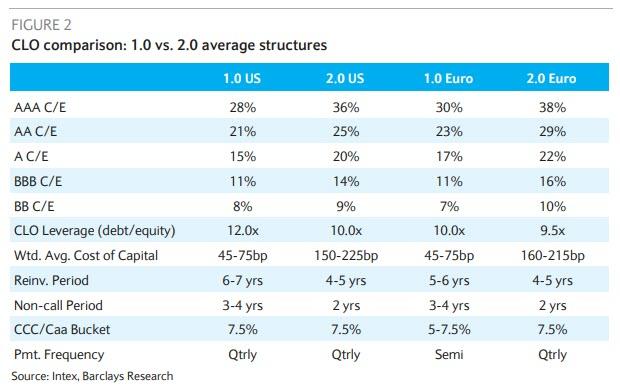

The CLOs 2.0 average structures (aka, “Cov Lite” loans) have higher risk.

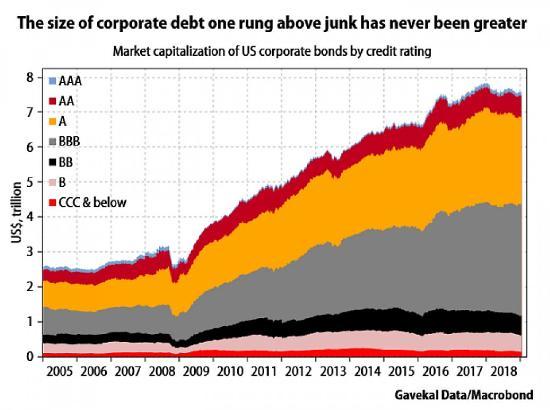

While this is NOT a chart of CLOs, it does show the growth of corporate debt since the financial crisis, particularly at the A and BBB ratings.

Makes one ponder holding a protective asset like … gold.

Here we are again!

Join the conversation and have a little fun at Capitalstool.com. If you are a new visitor to the Stool, please register and join in! To post your observations and charts, and snide, but good-natured, comments, click here to register. Be sure to respond to the confirmation email which is sent instantly. If not in your inbox, check your spam filter.